The DEFINE modelling framework has the following distinct features:

1. The economy is portrayed as an open subsystem of the closed ecosystem. It is explicitly taken into account that the production of goods employs useful energy and matter from the environment as inflows and generates significant amounts of material waste and greenhouse gas emissions that affect the stability of the ecosystem, having feedback effects on economic activity.

2. The economy-environment interactions respect the laws of thermodynamics: The restrictions that stem from the First and the Second Law of Thermodynamics (including the Law of Conservation of Mass) are explicitly incorporated in the transformation of energy and matter.

3. There is a clear distinction between stock-flow and fund-service resources: The stock-flow resources (such as fossil fuels and minerals) are materially transformed into what they produce (including by-products), can theoretically be used at any rate desired and can be stockpiled for future use. The fund-service resources (such as labour and capital) are those that are not embodied in the output produced, can be used only at specific rates and cannot be stockpiled for future use. The distinction between these two types of resources is significant because it demonstrates that production needs both of them: there is no possibility to substitute the one for the other, as is the case in conventional presentations of the production function.

4. Output is demand-determined but environment might impose supply-side constraints: Following the post-Keynesian tradition, output is determined by the demand for consumption and investment products. However, supply-side constraints might arise because climate change can cause damages that affect capital and labour or because finite natural resources might be exhausted in the very long run.

5. The dynamic interaction between monetary stocks and flows is coherently analysed: In the macroeconomy and the financial system the monetary stocks are the assets and liabilities of households, firms, commercial banks, the central bank and the government. Examples of assets and liabilities include the deposits of households, the government bonds and the loans of non-financial corporations. The monetary flows refer to various monetary transactions that take place in each month or year, such as the payment of wages, the repayment of debt, the collection of taxes by the government and the interest payments on loans. Using stock-flow consistent techniques, DEFINE formalises the dynamic interaction between stocks and flows in an explicit and consistent way, following the accounting principles.

6. The financial system is an important integral part of the macroeconomy: The financial system and its functions (bank lending, equity emission, bond pricing etc.) affect macroeconomic activity and, hence, environmental problems. The financial system also has an important impact on the financial feasibility of various types of green investment plans. Simultaneously, the macroeconomy influences the stability of the financial system. Since a healthy ecosystem is a precondition for a sustainable macroeconomy, the ecosystem indirectly determines the stability of the financial system.

7. Money is endogenous: Money is endogenously created when banks provide loans to households and firms. The central bank is not able to control the amount of money created in aggregate. The endogenously created money can support economic growth and green investment, but it can also lead to higher financial fragility and a more unequal distribution of income and wealth.

8. Income and wealth distribution matter: The distribution of income and wealth affects consumption and investment expenditures and, therefore, economic growth, the use of natural resources and pollution. Moreover, the financial system affects the way that income and wealth are distributed, having feedback effects on debt accumulation.

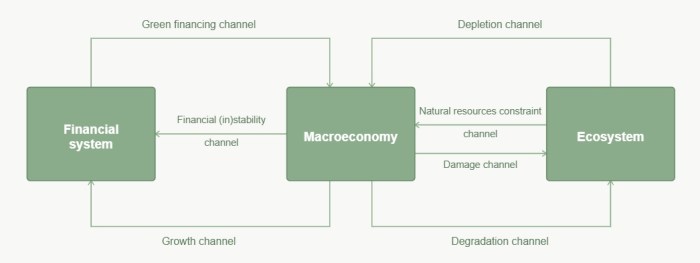

The main interactions between the ecosystem, the financial system and the macroeconomy in DEFINE are portrayed in Figure 1.

The DEFINE framework focuses on the following channels:

Degradation channel: Higher economic activity, which is accompanied by the use of matter and fossil energy, leads to CO2 emissions and the generation of hazardous waste. The overall result is the degradation of the ecosystem services due to the CO2-induced increase in atmospheric temperature and the harmful effects of waste accumulation.

Depletion channel: The extraction of matter and fossil energy sources that are necessary for the production process places upward pressures on the depletion ratios. In other words, economic growth tends to deplete finite natural resources.

Damage channel: The degradation of the ecosystem damages the fund-service resources (capital and labour) either by affecting them directly or by reducing their productivities. These damages might impose supply-side constraints on economic activity. The environmental damages also affect the behaviour of households and firms, which respond to these damages by cutting consumption and investment expenditures, respectively. As a result, aggregate demand falls, reducing economic growth.

Natural resources constraint channel: The depletion of natural resources reduces the availability of the stock-flow resources that are necessary in the production process (matter and fossil energy). This might impose supply-side constraints on economic activity.

Green financing channel: The financial system finances green investment via loans or bonds, contributing to the improvement of material intensity, energy intensity and recycling rates as well as to the increase in the use of non-fossil energy. Hence, the credit rationing and the interest rates determined by banks and central banks play an important role in the decoupling of economic growth from environmental problems.

Growth channel: The financial system has both positive and negative effects on economic activity. The positive effects include the provision of finance that increases investment and, hence, economic growth. The negative effects are related to the potential rise in firm leverage that, under certain conditions, can harm economic activity by reducing desired investment and credit availability.

Financial (in)stability channel: The stability of the financial system is affected by macroeconomic activity. However, the links are not clear-cut. On the one hand, high economic growth is conducive to the expansion of the financial system, which might be associated with higher financial fragility (reflected in higher leverage ratios). One the other hand, low economic activity creates debt repayment difficulties that affect the stability of the financial system.

For more details about the features and the foundations of DEFINE see here and here.